You are here

Alasdair Macleod: The gold leasing scam is over

This analysis was published Wednesday in Alasdair Macleod's financial letter at Substack and is republished here by his kind permission. Macleod's letter is published every few days and a seven-day free trial subscription is available. Rates are $10 per month or $120 per year. To subscribe, please visit:

https://alasdairmacleod.

* * *

By Alasdair Macleod

Wednesday, March 19, 2025

Before 2002 analyst Frank Veneroso estimated that between a third and half of all central bank gold had been leased or swapped, sold into the market and lost.

More recently, leasing centres such as the Bank of England transferred ownership from lessor to lessee by book entry transfer, the gold not normally leaving the vault. That changed with the recent panic, with lessees queuing up to take gold out of the bank's vault and ship it to New York.

... Dispatch continues below ...

... ADVERTISEMENT ...

Bullion Star Opens in the U.S., Selling and Vaulting Gold and Silver

Bullion Star is now open in the United States, offering gold and silver bullion at extremely competitive prices with free delivery. Bullion Star also offers customers a year of free vault storage along with free delivery as well as storage in its secure precious metals vault in Dallas, Texas.

Storing precious metals is challenging. Homeowner's insurance seldom covers precious metals, and safe deposit boxes offered by banks are neither insured nor covered by the government deposit insurance. Bullion Star's vault is an independently run, Class III UL-rated vault with uncompromising surveillance and round-the-clock security.

With Bullion Star you can transact and store your metals securely and confidentially. Your bullion is fully insured against all risks at full replacement value. Bullion Star uses five audit methods to verify the existence and correctness of your stored bullion.

For more information, please visit:

This article is about the gold leasing trade, and why the sudden return to conditions before the book-entry transfer system threatens a new liquidity crisis in spot markets.

... Gold leasing before 2002 ...

Following the abandonment of Bretton Woods in 1971, the U.S. Treasury embarked on an anti-gold campaign.

In the early days it was crude, consisting of anti-gold propaganda and very public auction sales into the market designed to kill investor appetite. The sales were swallowed up by eager buyers, so they were quickly stopped.

We don't know the extent of secret sales since then or if they even took place. The suspicion is that they did, and that the U.S. Treasury's stock of gold is considerably less than the 8,133-odd tonnes consistently reported for at least the last 25 years.

Subsequent to the early auctions, there was no need for these sales when the Treasury or its Exchange Stabilisation Fund could deal in the paper markets instead. Perhaps the Treasury has been content to misdirect everyone's attention away from the real trouble stored up for the future, which is the topic of this article.

Because of its consequences, the more serious manipulation is the additional physical supply into markets from gold leasing. It is serious because paper manipulation is short-term, while extra supplies of physical bullion are a long-term commitment, storing up trouble for the future when the truth is eventually revealed.

The evidence of this extra supply is unequivocal. Over 20 years ago, analyst Frank Veneroso reported:

"We estimated from BIS data that the total amount of the gross gold derivatives of the bullion bankers, all 37 of them, has been somewhat more than 40,000 tonnes. That would suggest something like 10.000 to 16,000 tonnes of gold have departed from the official sector as a result of official gold lending."

See: https://www.gata.org/node/5275

In his article Veneroso went on to examine gold leasing/lending by central banks from different angles and came to similar conclusions every time: that by 2002 between one third and one half of the reported 33,000 tonnes of central bank gold had gone AWOL.

Gold leasing had been going on for some time. Originally, a user of gold such as a jewelry business would lease a quantity of gold based on its estimate of demand for fabrication for a given period. It would then buy it forward so that at the end of the lease he could deliver it back to the lessor. This meant that the jeweler didn't have to buy the gold up front, and he effectively borrowed it.

In the early-1980s banks, shadow banks, and the emerging hedge fund industry got involved and the carry trade into high-yielding U.S. Treasury bills began. The London Bullion Market Association forward market rapidly expanded.

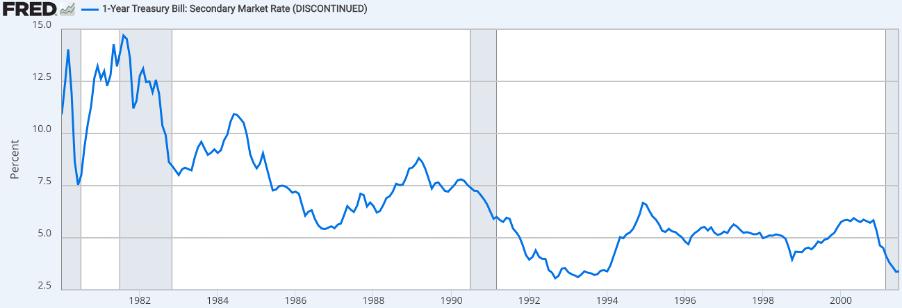

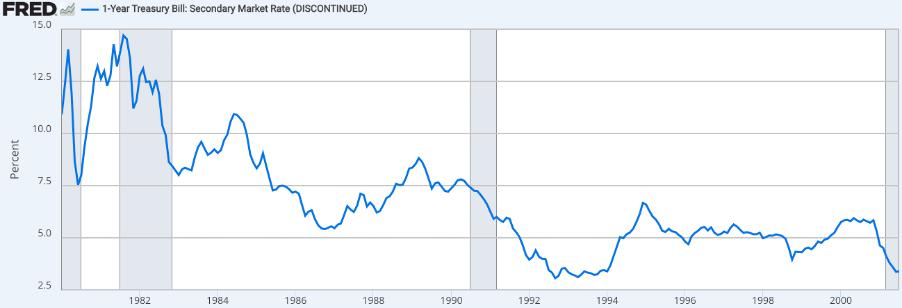

The attraction to hedge funds and shadow banks (such as Goldman Sachs, which was not a licenced bank in those days) was that they could lease gold at, say, 1%, and buy T-bills yielding considerably more, as this chart illustrates:

https://www.gata.org/sites/default/files/AlasdairMacleod-1.jpg

Particularly when leveraged, the returns over the lease rate were fantastic. It was the grandfather of all carry trades. But it required the leased gold to be sold to raise the dollars to buy the T-bills. Veneroso concluded that most of the leased gold sold was not repurchased and had disappeared into the market.

I do not see commercial banks necessarily being directly involved. They had no need to fund the liability side of their balance sheets by leasing gold because they merely created the credit to invest directly into U.S. T-bills. But gold leasing was a trade that gave impetus to the new hedge fund industry and other shadow banks not licenced to create bank credit.

The role of commercial banks' bullion bank subsidiaries was simply to make a market and trade in the over the counter forward contracts demanded by the shadow banks hedging their lease obligations.

Indeed, in this light the policies and attitudes of the LBMA can be better understood.

Like the jewelry trade pre-1980s, we can assume that these shadow banks would have bought contracts to cover their lease obligations. For example, if a hedge fund leases 10 tonnes of gold from a central bank for six months, it would be prudent to buy the same quantity of gold for forward settlement in six months' time.

That doesn't mean that on expiry of the lease the gold is delivered. With the agreement of the lessor, the lessee may be able to extend the lease, or it might sell the lease before it terminates. Or it could go to the Bank for International Settlements, the Bank of England, or the New York Fed, all of which managed lease contracts, to roll them over and not have to deliver.

It was the birth of a new gold-derivative industry centred in London, and central banks were keen to support it, given its income generation for them.

... As gold price fell, leasing became more profitable ...

The 1980-2002 period saw the gold price decline from the 1981 highs of over $800 to $250, adding to the general profitability of this lease trade and encouraging its growth. Importantly, it suited the U.S. Treasury, which was determined to remove gold from the international monetary system and replace it with the Fed's dollar. By increasing the supply of gold into the market, gold leasing served this purpose and helped fund the U.S. budget at the same time.

Things probably changed from the mid-'90s onwards, with leased gold remaining in the BIS, Bank of England, and New York Fed vaults, the change of possession from lessor to lessee being evidenced by book-entry transfer and a vault confirmation of a lessee's ownership. It meant that leased gold no longer needed to leave the vault where the original central bank owner had it stored. But it also meant that ownership of many of the bars recorded as the property of central banks were actually owned by commercial entities.

It probably explains why the New York Fed was reluctant to return Germany's gold when the Bundesbank requested the repatriation of some of its gold from the New York Fed's vaults. And more troublingly, it suggests that the New York Fed was leasing earmarked Bundesbank gold without the Bundesbank's agreement, which would explain why the returned bars did not match Bundesbank records.

The book-entry transfer system doesn't eliminate the earlier problem of gold disappearing from the system. It simply replaces it with dual ownership. Gold continues to be used for collateralised finance, particularly since Basel 3 classified it as a high-quality liquid asset for the purposes of bank balance sheet capital adequacy calculations.

This raises the question of what happens if for any reason the additional gold supply arising from dual ownership of central bank gold ceases and begins to reverse.

... As leased gold is returned, liquidity declines ...

This is particularly relevant because of the recent run on deliveries from the Bank of England's vaults destined for New York and reported deliveries out of Switzerland, to the extent that they involve gold held by the Bank for International Settlements. We can be almost certain that these deliveries are of leased gold, temporarily possessed by shadow banks but due to be returned to the ownership of central banks on expiry of their leases.

It should be emphasised that leased gold is the property of the lessee for the duration of the lease. If the lessee wishes to withdraw it from, say, the Bank of England's vault, it is free to do so. The recent significant premiums to spot on Comex was such a reason, creating a physical arbitrage sucking liquidity out of other gold trading centres as well as London. This chart shows the surge in stocks in Comex warehouses:

https://www.gata.org/sites/default/files/AlasdairMacleod-2.jpg

Since end-October, Comex warehouse stocks increased by 728.5 tonnes. The previous peak followed Covid lockdowns when a similar panic occurred. These are not normal levels.

Given the general lack of liquidity in global gold markets, the bulk of this is almost certainly central bank gold on lease. Indeed, according to Bank of England vault figures, between end-October and February, 260.4 tonnes were delivered out, and there will be more by the end of March. That probably leaves about half the surge in Comex warehouse stocks coming from elsewhere.

With gold surmounting $3,000 and foreign central banks becoming increasingly nervous of Trump's trade and U.S. monetary policies, the lessors might decide not to renew leases. This will have the effect of withdrawing physical supply from global markets at a time when portfolio reallocations are likely to increase demand for physical gold. Only one thing can happen: Prices will go higher until a new balance between supply and demand is found.

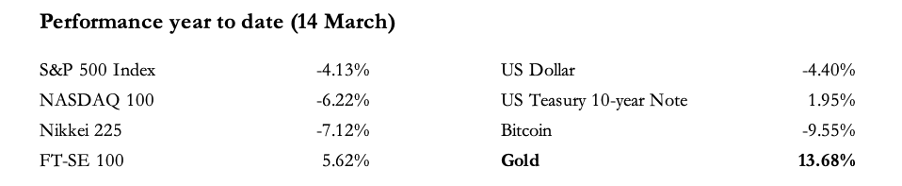

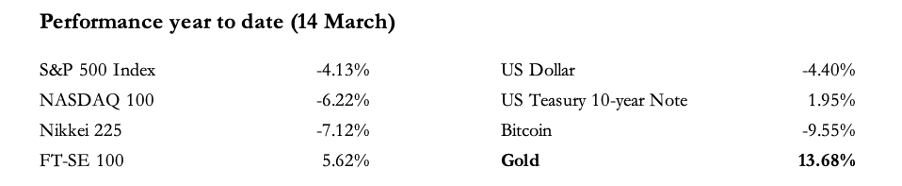

A very real danger in this is that gold will behave like a Giffen good, and that balance not be found. Demand increases as the price increases, because the entire investment universe of nearly $300 trillion is underweight in gold, gold exchange-traded funds, and gold mines. Gold is the best-performing asset class in Q1 this year and is bound to lead to portfolio rebalancing as other investment sectors are sold down. The table below illustrates this point to March 13, after which gold has risen even further:

https://www.gata.org/sites/default/files/AlasdairMacleod-3.png

No fund manager will want to show no gold and gold-related positions at the quarter end, which is only days away.

In that event, short positions that are half the entire paper gold universe of many billions of dollars will rush to close. Gold could even go bid-only with no sellers, signaling that the paper market leasing scam is over.

-----

Alasdair Macleod began his career as a stockbroker at the London Stock Exchange in 1970. Since then he has been an investment manager and an executive director of an offshore bank in Guernsey.

* * *

GATA is grateful to these companies for their recent support:

Apollo Silver Corp.

Barksdale Resources

Dolly Varden Silver Corp.

Dryden Gold Corp.

Group Eleven Resources

Guanajuato Silver

IBK Capital Corp.

Independent Trading Group

Mining Discovery

Power Nickel

Silver North

Strike Point Gold

The National Investor

The Prospector

Western Alaska Minerals

* * *

Support GATA by purchasing

Stuart Englert's "Rigged"

"Rigged" is a concise explanation of government's currency market rigging policy and extensively credits GATA's work exposing it. Ten percent of sales proceeds are contributed to GATA. Buy a copy for $14.99 through Amazon:

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

Donations of $250 will entitle the donor to a 1-ounce silver round commemorating GATA's work:

https://www.gata.org/sites/default/files/GATA-silver-round-front.png

| Attachment | Size |

|---|---|

| 26.78 KB | |

| 31.06 KB | |

| 28.87 KB |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}