You are here

Reg Howe - Current MPEG Commentary - Gold Derivatives: Hitting the IceBerg

Gold Derivatives: Hitting the Iceberg

What is the size of the total short physical gold position, or put another way, how much gold from their vaults have the central banks collectively deposited, leased or swapped into the market through the bullion banks? Taking advantage of guidelines promulgated by the International Monetary Fund, most central banks report their gold reserves without providing a breakdown between bullion held in their vaults and gold receivables owed to them on account of deposits, loans and swaps, as would be required under more normal accounting practice. Thus the size of the total short physical position continues to stir controversy, with Gold Fields Minerals Services sticking to its estimate of 4000 to 5000 tonnes notwithstanding the mountain of research by the Gold Anti-Trust Action Committee and its associates suggesting an amount two to three times as large. See, e.g., T. Wood, "That gold short position," Mineweb (December 5, 2003).

Summarizing material published by James Turk, Frank Veneroso and at this website, the above-cited article states: "Combining those figures [outflows of 'official' gold from the Bank of England as indicated by British export statistics uncovered by Mr. Turk] with the NY Fed and BIS data produces an outstanding gold loans number more or less in line with the original Veneroso estimates of 1998 and subsequent 'back-in' calculations by Reg Howe that put the figure at 15,000 tonnes."

My approach to estimating the size of the total short physical position tries to interpret the data on gold derivatives regularly published by the Bank for International Settlements. For the reasons discussed in Gold Derivatives: Moving towards Checkmate (12/04/2002), updated in Not Your Father's Gold Market (6/15/2003), total forwards and swaps as reported by the BIS are in my opinion a pretty good proxy for the total short physical gold position, especially since the BIS endeavors to eliminate the double counting that would otherwise result when reporting entities are on both sides of the same contract.

Unlike options, forwards and swaps are transactions which generally assume the sale of an equivalent amount of gold into the spot market. Bullion banks borrow gold, usually from central banks, for the purpose of acting as financial intermediaries. They sell the gold acquired by deposit, loan or swap, and then invest the proceeds in an effort to earn a positive spread while at the same time hedging themselves against any unfavorable movement in gold prices as, for example, by taking the other side of a forward sale by a gold producer or by purchasing call options.

Gold loans used to fund forward sales by a gold producers are typically repaid out of future mine production, and thus are integrated with a hedging transaction that is independent of the gold market. In contrast, gold loans used to fund what for several years was a very profitable gold carry trade required forward sales by non-producers that could be hedged only in the options market. Ultimately, unless settled in cash, these gold loans must be repaid by metal acquired in the market.

The controversy over the size of the total short physical gold position really boils down to a debate about the size of the gold carry trade relative to hedging by gold producers and traditional gold borrowing by the jewelry industry and other gold fabricators.

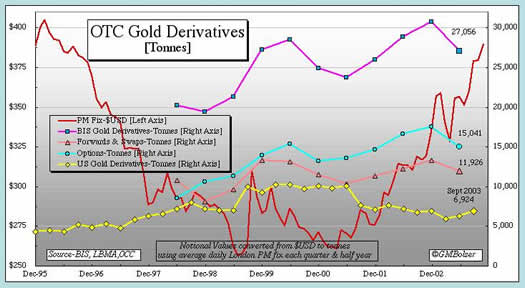

Most Recent Data on Gold Derivatives. On November 12, 2003, the BIS released its regular semi-annual report on the OTC derivatives of major banks and dealers in the G-10 countries for the period ending June 30, 2003 (www.bis.org/publ/otc_hy0311.htm). The total notional value of all gold derivatives, which had risen from $279 billion at mid-year 2002 to $315 billion by year-end, declined to $304 billion as of June 30 this year. Translated into estimated tonnes, these figures are shown in the chart below by Mike Bolser, together with the breakdown between forwards and swaps ($134 billion versus $136 billion at year-end 2002) and options ($169 billion versus $180 billion at year-end 2002) as reported in table 22A of the recently published December issue of the BIS Quarterly Review (www.bis.org/press/p031208.htm).

Also shown in tonnes are the gold derivatives held by U.S. commercial banks as of September 30, 2003, as reported by the Office of the Comptroller of the Currency (www.occ.treas.gov/deriv/deriv.htm). Held almost entirely by J.P. Morgan Chase, Citibank and HSBC USA, the total notional value of these gold derivatives rose in the third quarter to $80.9 billion from the roughly $70 billion level where they had been holding since year-end 2002. As can be seen from the breakdown by bank included in the GOLD MARKET REGRESSION CHARTS also updated today, the third quarter increases were spread across all three major U.S. bullion banks.

CLICK ON CHART TO VIEW LARGER VERSION

Tip of the Berg. Pierre Lassonde, Newmont's president, observed last July that when the Newmont/Franco-Nevada/Normandy merger was announced in November 2001, the total world producer hedge book stood at around 4000 tonnes, that since then it had fallen to 2400 tonnes, and that he expects it to continue to decline by 400 to 600 tonnes per year until stabilizing at around 1000 tonnes representing the borrowing requirements of the jewelry industry. See T. Wood, "Newmont scalps hedge cynics," Mineweb (July 31, 2003). Although casting some doubt on whether producer hedge book reductions are proceeding at the predicted pace, reports from Gold Fields Minerals Services are consistent with the historical figures cited by Mr. Lassonde.

The following table summarizes the data on total delta-adjusted producer hedge books presented by GFMS (http://www.gfms.co.uk/index.html) in the first four editions of its series on Global Gold Hedge Book Analysis (in millions of ounces except as otherwise noted):

Forwards Options Non-Vanilla Total Total

Products Ounces Tonnes

2001, Qtr. 4 73 15 6 94 2924

2002, Qtr. 4 59 16 4 80 2488

2003, Qtr. 1 55.2 16.2 3.5 74.9 2330

2003, Qtr. 2 53.5 14.6 3.5 71.6 2226

2003, Qtr. 3 53.0 15.2 3.5 71.6 2227

Note: Where figures for prior periods were adjusted in subsequent

editions, the revised figures have been used.

A comparison of this table with the figures from the BIS presents several issues meriting comment. But first a threshold issue relating to differences in reporting methodologies must be addressed. Notional values as reported by the BIS and converted to tonnes are not precise equivalents to "committed" or "protected" ounces as reported in some studies of producer hedging. But for all practical purposes, especially as regards forwards and swaps, the two measures are reasonably close. However, particularly with regard to options, notional value and "delta-adjusted" value are quite different, as the following example will illustrate. See, e.g., Virtual Metals Research, "Gold Mine De-hedging Steams Ahead, says Gold Hedging Indicator," Minesite.com (August 15, 2003).

If a producer writes a call for 100,000 ounces at $400/oz., the notional value of the call would be $40 million (100,000 times $400). However, depending on the spot gold price, its implied volatility, the duration of the call and other factors, including the prevailing level of interest rates, the delta on the call, i.e., the number of ounces needed to hedge the risk represented by the call, would be only a fraction of this amount. Thus, while the BIS shows options accounting for more than 50% of total gold derivatives whereas GFMS puts them at only around 15% of total delta-adjusted producer hedge books, it is quite possible that in fact these two percentages would be roughly equivalent if measured on the same basis.

With respect to forwards, the effects of delta-adjustment are not nearly as dramatic since, as GFMS explains in its Technical Annex to the series, "the forward delta [rate of change in the value of the derivative relative to a change in the price of the underlying reference unit] is l, whilst in the case of an option, this delta is derived from the Black-Scholes option pricing formula." Thus, as GFMS notes (Edition 3, August 2003, p. 7): "[T]he dominance of forward sales makes the size of the global delta-adjusted outstanding hedge book relatively insensitive to changes in spot gold prices and implied volatilities."

Even at 4000 tonnes, the world producer hedge book could never seem to account for more than about a third of the total forwards and swaps reported by the BIS. Now, with that number almost cut in half, total forwards and swaps as reported by the BIS remain marginally above their year-end 2001 level and not far off their year-end 2002 peak. Taking GFMS's delta-adjusted figures, the decline in producer hedge books is not quite as steep, but still amounts to a drop of nearly 700 tonnes or almost 25% since year-end 2001. Indeed, most of this decline (436 tonnes) came in 2002 when the BIS actually reported rising forwards and swaps.

Taken as whole, these numbers cast serious doubt on the widely-accepted assumption that producer hedging is responsible for the great bulk of total gold derivatives, particularly forwards and swaps. Notwithstanding the efforts of the BIS to eliminate double-counting, some have argued that its higher figures are the result of unspecified overlaps which have the effect of inflating producer hedging to much higher levels than those reported by GFMS. But if this argument were valid, reductions in producer hedge books should have operated in reverse to deflate the BIS's figures on gold derivatives by equally large amounts.

That producer hedge book reductions have had little if any impact on total gold derivatives reported by the BIS suggests, as does the absolute data itself, that producer hedging never accounted for much more than the very visible tip of a gold derivatives iceberg consisting in major part of transactions related to the gold carry trade, which never could have grown to the size implied by the BIS data without the active support of the G-10 central banks.

Ocean of Currency and Credit. Historically, the principal monetary function of gold has been to stabilize both currency values and interest rates. See Interest Rates: The Golden Connection (12/27/1999). In recent years, the major central banks, led by the U.S. Federal Reserve, have allowed and encouraged gold derivatives to grow far beyond prudent limits in an effort to silence the monetary alarm that rising gold prices would otherwise have sent as they flooded the world with paper money and loose credit. See Gibson's Paradox Revisited: Professor Summers Analyzes Gold Prices (8/13/2001).

The following chart by Don Lindley updates earlier versions that have appeared in prior commentaries. It pretty much speaks for itself, but recently for the first time in the 45 years covered by the chart the absolute size of the M-2 and and the M-3 money supplies has fallen. What this unprecedented development may portend is unclear, especially at this early stage, but among the more worrisome possibilities is a finite and now shrinking demand for dollars.

CLICK ON CHART TO VIEW LARGER VERSION

Floating on this ocean of unlimited paper, the gold derivatives iceberg threatens a collision with reality that could sink the global financial system and the "Titanic" of paper currencies on which it rests, the U.S. dollar. As the passengers and crew on the original Titanic discovered, even a glancing, barely perceptible encounter with an iceberg can inflict a mortal wound not immediately apparent to the casual observer or even to the trained eye absent a complete damage assessment.

Thus, but for the publicly revealed private comments of Eddie George, former Governor of the Bank of England, the first potentially lethal scrape with the gold derivatives iceberg might never have come to light. See Complaint in the Gold Price Fixing Case, paragraph 55. Sharply rising gold prices triggered that incident, and the question today is whether their recent rally to over $400/oz. is in the process of precipitating another derivatives disaster.

Below the Waterline. Each Friday the Commodity Futures Trading Commission (www.cftc.gov/cftc/cftchome.htm) releases a Commitments of Traders Report (www.cftc.gov/cftc/cftccotreports.htm) providing details on the composition of positions held as of the preceding Tuesday by futures traders in each commodity so traded on U.S. exchanges. The COT data is broken down into reportable and non-reportable positions, i.e., those below certain defined limits and usually attributed to small speculators. The larger reportable positions are further categorized as either commercial or non-commercial. Reportable commercial positions are typically those of producers, end-users, hedgers, banks and other financial intermediaries. Reportable non-commercial positions are typically those of commodity funds and other large investors and speculators.

Experience suggests that the commercials are usually better than the large specs and funds at anticipating major turns in the market. Consequently, a so-called "commercial signal failure" -- a major move that catches the commercials heavily on the wrong side of the market -- is a relatively rare event. As the chart below by Don Lindley shows, since 1985 spikes in open interest held by commercial shorts have typically preceded major downdrafts in gold prices. As the chart also reveals, non-commercial longs have held the other side of a substantial proportion of these contracts, but have also been rather quick to cut their losses.

CLICK ON CHART TO VIEW LARGER VERSION

Since 2001, open interest in COMEX gold futures has moved sharply higher along with rising gold prices. These trends have been accompanied by equally sharp increases in the open positions of the commercial shorts and the non-commercial longs. Indeed, as the chart indicates, open interest in COMEX gold futures is at its highest level since 1984, as are the open positions of the commercial shorts and non-commercial longs as well.

Recently a professional off-the-floor COMEX gold trader published an analysis estimating that from October 14, 2003, when COMEX gold closed at $377, to December 2 when it closed at $404.60, the commercial shorts accumulated unrealized losses of over $480 million on their nearly 216 million open gold futures contracts representing more than 670 tonnes. See D. Norcini, "Hot Shot Commercial Losers on the COMEX," LeMetropoleCafe (December 7, 2003). What is more, Mr. Norcini has advised me in private correspondence that the same analysis from the beginning of August when COMEX gold closed at $351 puts their losses at nearly $1 billion.

Clearing house rules require that losses to trading accounts be posted each day at settlement. Losses of the size incurred by the commercial gold shorts over the past few months beg two tough questions: What risk management system would allow losses of this magnitude to accrue without mandating the closure of losing positions? And are the central banks, directly or indirectly, assuming the burden of these losses?

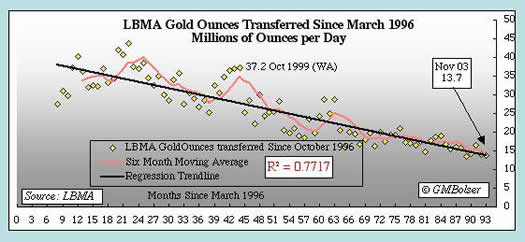

In contrast to rising open interest on the COMEX, average daily gold turnover on the London Bullion Market Association continues to decline, as illustrated in the following chart by Mike Bolser. In practice, COMEX futures contracts are generally settled by cash payments rather than physical delivery. The LBMA, although also largely a paper market, executes a significant number of transactions for physical delivery. Considerable anecdotal evidence suggests that physical demand has remained quite robust even at prices over $400/oz.

Under these circumstances, anyone selling gold for the purpose of holding down prices is well-advised to do so in New York after the London market has closed, thereby reducing the opportunity for buyers of scarce physical metal to take advantage of the lower prices. However, the transfer of so much trading volume to the COMEX at the apparent expense of the LBMA suggests that physical buyers may have turned this tactic to their own advantage, and raises the odds that at some future date the COMEX could face sharply higher demands for physical delivery.

Another possible and/or partial explanation for these diverging trends in gold trading volumes on the COMEX and LBMA is hinted at in the recent data on gold derivatives. The BIS lumps all exchange-traded derivatives as a single memorandum item and excludes them from its totals. The OCC, however, includes exchange-traded as well as OTC contracts in its detailed figures on gold and other derivatives. It says that approximately 10% of the total derivatives covered by its reports are exchange-traded, but does not break them out for each derivatives category.

Nevertheless, it is interesting to note that while gold derivatives reported by the BIS declined slightly in this year's first half, the gold derivatives of U.S. commercial banks, including J.P Morgan Chase, rose in the second and third quarters by nearly 1000 tonnes. These increases, which came at the same time that the commercial shorts on the COMEX were raising their open positions to record levels notwithstanding eye-popping mark-to-market losses, lend further support to the hypothesis that the commercial shorts consist primarily of bullion banks with both heavy exposure to the gold carry trade and substantial official support.

View from the Bridge. Earlier this month at a gold conference in Dubai, Giacomo Panizzutti, former chief gold trader at the BIS and until his retirement last year the official responsible for policing compliance with the Washington Agreement on Gold, predicted that the five-year agreement would be renewed for another five-year term when it expires next fall. See G. Ghantous, "Higher central bank gold sales likely, former BIS gold executive says," Reuters (December 6, 2003). What is more, he expects that the limit on sales over the next five-year period will be raised to between 2300 and 2400 tonnes from the present 2000 tonnes, and he "would not be surprised if they were to abandon the restriction on gold lending."

As announced on September 26, 1999, paragraph 4 of the WAG provided: "The signatories to this agreement have agreed not to expand their gold leasings and their use of gold futures and options over this period." Absent from this sentence was any mention of swaps, and soon thereafter the IMF changed its accounting and reporting conventions to allow gold swaps to be treated in the same manner as gold loans notwithstanding significant legal distinctions between the two. See, e.g., Statistics Department, International Monetary Fund, "The Macroeconomic Statistical Treatment of Reverse Transactions" (Thirteenth Meeting of the IMF Committee on Balance of Payments Statistics, Washington, D.C., October 23-27, 2000). As a result of these accounting shenanigans, compliance with the WAG's limitations on gold lending and the use of futures and options could never be independently verified.

Any elimination of restrictions on gold lending would likely reflect a belated recognition that the practice had exceeded prudent limits. Indeed, it is quite possible that the central banks have finally reached the outer limits on how much gold they are prepared to put at serious risk of loss. Incentives for gold lending have also been reduced by low lease rates, which cannot exceed interest rates without putting gold prices into backwardation. See discussion in The Golden Sextant (1991) and War against Gold: Central Banks Fight for Japan (1999).

In any event, with gold producers cutting back their hedge books and the gold carry trade crippled by both low interest rates and the rising trend in gold prices, the prospects for growth in gold lending appear bleak. Indeed, a growing inability to find willing gold borrowers may help to explain the record level of commercial shorts in COMEX gold futures, which unlike OTC forwards and swaps do not ordinarily involve an initial sale of physical gold obtained from a central bank.

As to specific countries that are probable or potential sellers during the next round, Mr. Panizzutti named Germany, Switzerland, Spain, and rather surprisingly France, but excluded "further sales" from Britain, Sweden or Italy. Germany, of course, has trumpeted its intention to sell gold so often that the market savvy participants no longer pay much attention. Many assume that future sales by the Bundesbank will for the most part represent cash settlements of previous gold loans or swaps rather than new metal being injected into the market.

The use of the adjective "further" in connection with Italy is strange since that nation was not allocated any sales under the WAG. Nor from the date of that agreement through last October had Italy reported any reduction in its gold reserves of 78.83 million ounces (2452 tonnes) declared to the IMF. Perhaps what Mr. Panizzutti meant to say is that any sales by Italy will not represent further gold hitting the market but, as is likely with Germany, prior loans or swaps being finally closed out as sales.

With respect to his prediction of French gold sales, Mr. Panizzutti is more likely playing mind games with the market and/or the French than disclosing any new intelligence about the intentions of this traditionally gold-friendly nation, which reports over 3000 tonnes of gold in its official vaults and thus may well possess the largest unencumbered hoard of physical gold on the planet. Perhaps he thinks that the former head of the Banque de France in his new position as head of the European Central Bank will be more amenable to calling on French gold to try to rescue modern central banking from its own mistakes. However, in banking as at sea, there are situations in which salvation requires more than simply manning the pumps.

According to the latest statistics on the WAG from the World Gold Council, the absolute limit of 2000 tonnes for the whole five-year period limits total sales during this last year of the WAG to 385 tonnes, of which Switzerland is expected to account for 284 and the Netherlands for 95. Swiss sales under the WAG have proceeded at a fairly steady pace, but as shown in the chart by Don Lindley below, sales by member nations of the ECB have taken place on an erratic basis, often bunching up during periods of high or rising gold prices as in the past several weeks.

CLICK ON CHART TO VIEW LARGER VERSION

Heart of the Ocean. In the actual event, the "Heart of the Ocean" was not aboard the RMS Titanic. That famous diamond, like the saga of Rose and her competing lovers, was created for the movie version. But life often imitates art, and truth can be stranger than fiction. As the world financial system built around the paper dollar collides with the gold derivatives iceberg, the glittering jewel starring in the most intriguing subplot is Barrick Gold, the company that used some of the planet's greatest gold ore bodies to create its most notorious producer hedge book. See R.K. Landis, Readings from the Book of Barrick (5/15/2002) and Readings from the Book of Barrick: the Sequel (11/27/2002).

Facing a deeply underwater hedge book of 16 million ounces (approximately 500 tonnes) and a lawsuit charging that the company and its bullion banker, J.P. Morgan Chase, had used forward sales to manipulate gold prices, Barrick recently announced that it would discontinue its gold hedging program and bring its hedge book down to zero. See T. Wood, "Barrick bows to 'today's investment climate,'" Mineweb (December 2, 2003). Details on how Barrick will achieve the latter objective are scanty, but options have been mentioned. See N. Mordant, "Barrick adopts no-hedging policy, says it aims to close its hedge book," Reuters (December 2, 2003).

Barrick's announcement followed an embarrassing public turnabout by its founder and chairman, Peter Munk, who after delivering a stout defense of the company's hedging program to a London gold conference one day, returned to the podium the next to declare the program dead. See K. Gooding, "Now Barrick hedge will be dropped," Mineweb (November 24, 2003). Providing even more grist for speculation, Mr. Munk was the replacement speaker for Barrick's new CEO, Greg Wilkins, who reportedly had urgent business in New Orleans, the venue of the lawsuit, which is scheduled for trial next April even though discovery has just recently begun.

In addition to damages, the plaintiffs, led by Blanchard and Company, the largest retail dealer in physical gold in the United States, have asked for an injunction "terminating all Master Trading Agreements, spot deferred sales contracts and all other contracts through which Defendants manipulate the market for gold as alleged herein, on terms that provide for the expeditious repayment of the borrowed gold [emphasis supplied], and enjoining Barrick, J.P. Morgan and [other unknown corporations] from entering into such contracts in the future." Third Amended Complaint, para. 126(a) (copy online at https://www.savegold.com/litigation.html#).

Not surprisingly, there has been considerable speculation with regard to what may be going on behind the scenes. For whatever reason, Barrick has effectively met the second part of the plaintiffs' demand for injunctive relief. However, satisfying the first part -- the closure and repayment of existing spot deferred contracts on an "expeditious" basis -- is not as easy to accomplish. Five hundred tonnes is a lot of gold to pull from a tight physical market without giving prices a big push higher.

Large as it is, however, this amount hardly begins to melt the gold derivatives iceberg. This alarming fact lends Mr. Panizzutti's comments about future central bank gold sales the ring of a ship's officer trying to calm fears and maintain order while loading the lifeboats.

Sauve Qui Peut. Every man for himself. So begins the last act of most shipwrecks and other great disasters, and the final tests that reveal the true characters of the players.

The gold community has prospered more than most over the past year. And having endured years of oppression by government, not to mention ridicule by establishment figures of all stripes and colors, gold bugs have earned the right to enjoy their good fortune. But real gold bugs are not profiteers. They are freedom fighters. For them, securing their own financial survival and that of their families is important but not sufficient, for they dream of a world in which gold is again the international monetary numéraire and where all peoples and nations meet on a level economic playing field characterized by free markets and an absence of malignant government intervention.

November 25, 2003. Amended Class Action Complaint Filed in Kinross Litigation

The original Class Action Complaint in the litigation against Kinross Gold Corporation and related parties over Kinross's tender offer for the Kinam Preferred and related matters was filed on April 26, 2002, in the U.S. District Court for the District of Nevada in Las Vegas. On May 22, 2002, a second action against the same defendants relating to the same matters was filed in the same court. The defendants filed answers in June and August. On August 7, 2002, the Court entered an order consolidating the two actions, appointing the plaintiffs in the original action as lead plaintiffs, and approving their selection of their counsel as lead counsel.

On October 22, 2002, the plaintiffs filed a motion for class certification. A few days later, on or about October 28, the defendants filed a motion for judgment on the pleadings requesting the Court to dismiss count IV, which alleged securities fraud in violation of federal law, for failure to meet the strict requirements for pleading such claims mandated by the Private Securities Litigation Reform Act of 1995.

The plaintiffs filed a first set of written interrogatories to the defendants on December 8, 2002. The defendants responded in part by asserting that under the PSLRA their motion for judgment on the pleadings, notwithstanding that it addressed only one of the six counts in the Complaint, operated to stay all further proceedings in the case. These issues were then briefed by the parties and submitted to the Court.

On January 15, 2003, the Magistrate Judge ordered a stay of all discovery until the Court ruled on the motion for judgment on the pleadings on count IV. The stay of discovery was upheld by the District Judge on September 22, 2003. At the same time, he denied without prejudice the plaintiffs' motion for class certification, and granted the plaintiffs leave to file a new motion for class certification after resolution of the defendants' motion for judgment on the pleadings on count IV.

By an order entered on October 1, 2003, the District Judge dismissed count IV but granted the plaintiffs "leave to amend their Complaint as to a securities fraud claim within thirty (30) days of the entry of this order." By agreement of the parties and with the approval of the Court, this deadline was extended to November 21. Accordingly, last Friday the plaintiffs filed an Amended Class Action Complaint, which amends their securities fraud claim under federal law to provide more details in the format directed by the Court. What is more, the Amended Complaint also alleges various additional facts unknown to the plaintiffs as of the date of their original Complaint but subsequently revealed in disclosure documents relating to the Kinross/Echo Bay/TVX merger announced in June 2002 and completed in January 2003.

October 1, 2003. New Essay re Canada, Quebec and Gold

No one likes to contemplate the impending collapse of the U.S dollar-based international financial system. Similarly, Canadians on all sides of the debate often prefer to avoid dicussion of the constitutional divide that separates Quebec from the rest of Canada. These issues and how they relate to each other are the subject of a new essay posted today in Canada's two official languages. The original English language version is Saving Canada with Gold Grams. Its French language translation is posted under the intentionally provocative title: Québec Libre: Gramme par Gramme.

In the preparation of this essay, I have benefitted from the advice of partner Bob Landis, the chart-making talents of Mike Bolser, and very helpful comments and other input from two Canadiens. Don Jack, an eminent Toronto barrister, aided me in finding my way through the relevant Canadian legal and constitutional authorities, which at first glance present something of a maze to an American lawyer. Pierre-Jean Lafleur, a professional mining engineer based in his native Montreal, pulled together the data on Canadian gold production, assisted with some of the research in French language sources, and did almost all of the translation. Of course, the views and opinions expressed in the essay, as well as any errors of fact or other mistakes, are mine alone, and neither Don nor Pierre-Jean should in any way be held responsible for them.

October 1, 2003. Nouvel essai concernant le Canada, le Québec et l'Or

Personne ne souhaite voir l'effondrement imminent du système financier international basé sur le dollar des É.U. Pareillement, les Canadiens de tous les côtés du débat préfèrent souvent éviter la discussion à propos de la division constitutionnelle entre le Québec et le reste du Canada. Ces questions et comment elles sont reliées ensemble sont le sujet d'un nouvel essai affiché aujourd'hui dans les deux langues officielles du Canada. La version originale en langue anglaise s'intitule Saving Canada with Gold Grams. Sa traduction en langue française est affichée sous le titre intentionnellement provocateur de Québec Libre: Gramme par Gramme.

Dans la préparation de cet essai, j'ai bénéficié des conseils de mon associé Bob Landis, des talents en graphisme de Mike Bolser, et des commentaires très utiles et d'autres matériels venant de deux Canadiens. Don Jack, un avocat éminent de Toronto, m'a aidé à trouver mon chemin à travers les références canadiennes légales et constitutionnelles pertinentes, qui à première vue ressemble à un labyrinthe pour un avocat américain. Pierre-Jean Lafleur, un ingénieur géologue basé dans son Montréal natif, a assemblé les données sur la production d'or canadienne, il a assisté avec une partie de la recherche des références en langue française, et il a fait presque toute la traduction. Bien entendu, les points de vue et les opinions exprimés dans cet essai, comme toute erreur factuelle ou autres, sont entièrement miennes, et ni Don ni Pierre-Jean ne devraient être tenus responsable d'aucune façon pour elles.

August 29, 2003. Stolen Minutes (Bob Landis, Fence)

Bob Landis has just returned from vacation, where through questionable means he uncovered the Confidential Minutes of a recent meeting of the IMF board, a shadowy international monetary organization with big plans for radical restructuring of the global monetary system.

July 4, 2003. Monetary Independence: Reinventing the Wheel of Misfortune

"Does the Global Economy Need a Global Currency?" This question was put last week to invited participants attending Nobel laureate Robert Mundell's 10th Santa Colomba Conference at his Tuscany villa. See Robert L. Bartley, "World Money at the Palazzo Mundell," The Wall Street Journal (June 30, 2003).

The question seems timely today only because monetary sovereignty -- or, more accurately, monetary manipulation -- is confused with national independence, as demonstrated not only by British reluctance to join the euro area but also by the failed currencies of so many new or emerging nations. Nothing better illustrates the bankruptcy of the current world monetary system than the United States resorting to printing new Saddam dinars for Iraq. See Andrew Marshall, "U.S. forced to print Saddam banknotes," Reuters (June 9, 2003)

Jim Rogers has driven around the world twice, first on a motorcycle and more recently in a specially built Mercedes, always on the lookout for sound investment opportunities. Contrasting hyperinflation in Ghana and crummy currencies in other former British colonies in Africa with the CFA (Communauté Financière Africaine) franc, the peripatetic investor who co-founded the Quantum Fund with Gorge Soros observes (J. Rogers, Adventure Capitalist (Random House, 2003), p. 166):

The former French colonies may have wretched economies at times, but they do have sound currencies. Capital will flow to economies where investors know the currency will not decline in value. Such strict management and the fact that the CFA franc is now tied to the euro have made the African currency stronger, and that strength bodes well for the future of their economies. The fourteen countries are even investigating the possibility of establishing a free-trade zone.

For more on the CFA franc, see J. Irving, "For better or for worse: the euro and the CFA franc," Africa Recovery (United Nations, April 1999); and D. Stasavage, "When Do States Abandon Monetary Discretion: Lessons from the Evolution of the CFA Franc Zone," in J. Kirshner, ed., Monetary Orders (Cornell Univ. Press, 2003).

Exclusively territorial or national currencies dependent on legal tender laws and appealing to national identity are in fact a relatively recent development. See E. Helleiner, The Making of National Money (Cornell Univ. Press, 2003). Fortunately for Britain's thirteen American colonies, the two leading architects of their independence did not labor under any false illusions about unlimited paper money as an essential, viable, or even desirable attribute of the new nation's sovereignty.

Adams and Jefferson on Money. At common law prior to the Revolution, coining money was an act of sovereign power by the Crown; the money of England had to be either gold or silver of a given standard of fineness -- the true standard -- called sterling metal; and the Crown could not lawfully debase the value of coined money below the sterling standard. 1 W. Blackstone, Commentaries on the Laws of England (Amer. ed., 4 vols., 1771-1773), pp. 276-278.

By the act of 1750 in Massachusetts, local currency was set at 1.333:1 against sterling. See J.B. Felt, An Historical Account of Massachusetts Currency (Perkins & Marvin, 1839), pp. 127-128. This rate equated to that proclaimed by Queen Anne in 1704 and confirmed by Parliament in 1707 making one Spanish milled dollar equal to six local shillings in the colonies, compared to the English rate of 4.5 shillings based on silver content. At the time of the Revolution, Spanish dollars circulating in America contained on average approximately 375 grains of silver.

Anti-British sentiment led to the dollar being adopted in the Constitution as the monetary unit of the United States. Under the Coinage Act of 1792, which also made debasement a capital offense, the weight of the standard dollar was set at 371.25 grains of silver, or $1.29 per ounce. In 1834, the gold weight of the dollar was reduced from 24.75 grains of pure gold ($19.39/ounce) to 23.22 grains ($20.67/ounce) to equalize the mint ratio with the market ratio of silver to gold, the latter by operation of Gresham's law having fallen out of circulation. At that time, both metals were standard money, but the silver dollar remained the standard dollar and standard of value. See A.H. Hansen et al., Principles of Economics (Ginn, 1929), pp. 322-324.

Originally adopted in 1780 and 1784, respectively, the existing constitutions of both Massachusetts and New Hampshire predate the federal constitution and were adopted by and for the people of sovereign and independent states. John Adams drafted the Massachusetts Constitution, from which the New Hampshire Constitution then drew extensively.

Both these constitutions contained a silver clause: "In all cases where sums of money are mentioned in this constitution, the value thereof shall be computed in silver at six shillings and eight pence per ounce." Mass. Const., Pt. 2, ch. 6, Art. III; N.H. Const., Pt. II, Art. 97 (deleted 1950). At this rate, one shilling amounted to .15 of a silver ounce and one pound to three silver ounces or 3.85 Spanish dollars. In Massachusetts, although all property qualifications for electors and certain office holders to which the silver clause applied were long ago repealed, the clause itself remains in place today.

On December 15, 1778, John Adams wrote to Mrs. Warren (IX Works of John Adams, p. 475):

A paper currency, fluctuating in value, will ever produce appearances in the political, commercial, and even the moral world, that are very shocking at first sight; but, upon examination, they will not be found to proceed from a total want of principle, but, for the most part, from necessity.

Who will take the helm, Madam, and, indeed, who will build the ship, I know not. But of one thing I am well convinced, that a great part of the evils you mention arise from the neglect to model the Constitution and fix the Government.

Two months later, on February 25, 1779, he wrote to James Warren (II The Warren-Adams Letters (Mass. Hist. Soc., 1925), p. 89):

The only Enemy, of any great Consequence which is left to Us is our Currency. ...

What C[ongress] will do with the Paper I dont know, but they had better, by a Vote annihilate it all, or call it to be burned, infinitely, and go over the same ground again ten times than that G.B. should prevail. Burn it all with my good Will. My share shall go to the Flames with utmost cheerfulness. call it all in, in a Loan if you will, but then dont let it stand at Sterling Standard to be redeemed. This would be greater Injustice than to burn it all.

This vile Paper discourages and disheartens the Whiggs, and emboldens the Tories, more than it ought. blow it away, any way. Many have a Prejudice, that our Independance is connected with it. Convince both sides that our Independance dont depend upon that. That our Plate, our Stocks and all shall go rather than our Sovereignty depend upon it. It is worth them all and more, nay our Houses and Farms into the Bargain.

The relationship of pounds sterling, real dollars and continental dollars, which were never a legal tender, is illustrated is a letter dated October 26, 1780, from Adams to Mr. Calkoen (VII Works of John Adams, pp. 299-300):

The quantity of paper bills in circulation on the 18th of March last, was two hundred millions of paper dollars.

The congress then stated the value of it, upon an average, at forty for one; amounting in the whole to five millions of silver dollars, or one million and a quarter sterling. This they did, by resolving to receive one silver dollar in lieu of forty paper ones, in payment of taxes. This was probably allowing more than the full value for the paper; because, by all accounts, the bills passed from hand to hand, in private transactions, at sixty or seventy to one.

John Adams and Thomas Jefferson died on July 4, 1826, the fiftieth anniversary of the Declaration of Independence. Political foes during many of the intervening years, they reconciled in their last years through an extraordinary correspondence, described in part by John Adams in the following letter that reveals their shared views on the subject of paper money (X Works of John Adams, p. 376):

I am old enough to have seen a paper currency annihilated at a blow in Massachusetts, in 1750, and a silver currency taking its place immediately, and supplying every necessity and every convenience. I cannot enlarge upon this subject; it has always been incomprehensible to me, that a people so jealous of their liberty and property as the Americans, should so long have borne impositions with patience and submission, which would have been trampled under foot in the meanest village in Holland, or undergone the fate of Wood's halfpence in Ireland. I beg leave to refer you to a work which Mr. Jefferson has sent me, translated by himself from a French manuscript of the Count Destutt Tracy. His chapter "of money" contains the sentiments that I have entertained all my lifetime. I will quote only a few lines from the analytical table, page 21. "It is to be desired, that coins had never borne other names than those of their weight, and that the arbitrary denominations, called moneys of account ... had never been used. But when these denominations are admitted and employed in transactions, to diminish the quantity of metal to which they answer, by an alteration of the real coins, is to steal; and it is a theft which even injures him who commits it. A theft of greater magnitude and still more ruinous, is the making of paper money; it is greater, because in this money there is absolutely no real value; it is more ruinous, because, by its gradual depreciation during all the time of its existence, it produces the effect which would be produced by an infinity of successive deteriorations of the coins. All these iniquities are founded on the false idea, that money is but a sign."

As the Money Wheel Turns. American experience with the continental currency failed to deter either France or Germany from even more disastrous experiments with unlimited paper money. The sad saga of the French assignats is discussed briefly in a prior commentary, Randy Randite OutLaw: Another Perspective on Alan Greenspan, which quotes heavily from Andrew Dickson White's Fiat Money Inflation in France, first publicly read to an audience of senators and congressmen in Washington on April 12, 1876, to encourage support for full de jure restoration of the gold standard.

More recently, the activities of the Greenspan Fed have inspired others to recommend Constantino Bresciani-Turroni's definitive study of the German hyperinflation, The Economics of Inflation (Augustus M. Kelley, 1937; reprinted 1968). See, e.g., Marc Faber, "The Financial Implications of Reflation," The Gloom, Boom & Doom Report (June 23, 2003). More than a century separated the hyperinflations of France and Germany, yet Professor Bresciani-Turroni's conclusion (at p. 404) echoes White's in all essential respects:

The inflation retarded the crisis for some time, but this broke out later, throwing millions out of employment. At first inflation stimulated production because of the divergence between the internal and external values of the mark, but later it exercised an increasingly disadvantageous influence, disorganizing and limiting production. It annihilated thrift; it made reform of the national budget impossible for years; it obstructed the solution of the Reparations question; it destroyed incalculable moral and intellectual values. It provoked a serious revolution in social classes, a few people accumulating wealth and forming a class of usurpers of national property, whilst millions of individuals were thrown into poverty. It was a distressing preoccupation and constant torment of innumerable families; it poisoned the German people by spreading among all classes the spirit of speculation and by diverting them from proper and regular work, and it was the cause of incessant political and moral disturbance. It is indeed easy enough to understand why the record of the sad years 1919-23 always weigh like a nightmare on the German people.

The American, French and German inflations were aberrations from the reigning monetary orthodoxy. The classical gold standard, which prevailed from the early eighteenth century through the First World War, was relaxed at the Genoa Conference in 1922 to permit central banks to include currencies exchangeable for gold as part of their own gold reserves. This gold exchange standard, which in effect allowed the same gold to do double duty, collapsed in 1931 when Britain completely abandoned the gold standard.

During the 1932 presidential campaign, both parties promised to keep the United States on the gold standard. However, within days of assuming office in March 1933, President Roosevelt closed the banks, took the country off gold, banned most private ownership of gold, and nullified the gold clauses in all private and government contracts. These measures were followed in 1934 by devaluation of the dollar from $20.67 to $35.00 per ounce of fine gold.

The demise of the gold standard, effectively formalized by the collapse of the London World Economic Conference in 1933, is best told in The Money Muddle (Knopf, 1934) by James P. Warburg, who resigned as the president's chief monetary advisor in protest to his "monetary experimentation, deliberate inflation [and] economic nationalism." See The Coming Currency War: Roots. Conferring with a group of senators about the resolution nullifying gold clauses even in government obligations, FDR asked Oklahoma's Thomas P. Gore for his view. Senator Gore replied: "Why, that's just plain stealing, isn't it Mr. President?" See B.M. Anderson, Economics and the Public Welfare (Liberty Press, 1979).

Under the monetary measures of the New Deal, gold could be exported to approved central banks and governments upon presentation of dollars to the Federal Reserve. This system, adopted and confirmed by the Bretton Woods Agreements in 1944, lasted until President Nixon closed the gold window in 1971, breaking yet another solemn monetary commitment of the United States and ushering in the modern regime of floating exchange rates with an unlimited paper dollar as the key reserve currency, but now under serious challenge from the euro and soon perhaps from the gold dinar and Chinese renminbi as well. See Burning Bush: Pouring Oil on the Gold Wars.

Professor Mundell, widely regarded as the driving intellectual force behind the euro, has long urged reform of the international monetary system, often with a kind word for gold. See The Coming Currency War: Europe Prepares. As an economist with the International Monetary Fund, he had a ringside seat from which to observe the breakdown of the Bretton Woods system, and in 1969 the savvy Canadian native purchased the Palazzo Mundell as a hedge against inflation. From this palace five centuries earlier, Pandolfo "Il Magnifico" Petrucci had ruled Siena with skills that drew praise from Machiavelli in The Prince, particularly as regards his choice of advisors.

Were Machiavelli writing today, he might well have entitled his famous work The Central Banker. No other public officials operate with as little legal or effective political restraint, as much guile, or a firmer belief that their ends justify their means.

In Alan We Trusted. As the horror of the Great War's trench warfare and the postwar flu pandemic gave way in America to the Roaring '20s, trust in the dollar's gold redeemability stood in marked contrast to confidence in the national sport.

In Chicago's Cook County courthouse, a grand jury was convened to investigate reports that several White Sox players had conspired to throw the 1919 World Series. Leaving the courthouse after his testimony, legend records that "Shoeless" Joe Jackson -- one of the game's greatest hitters -- was approached by a small boy pleading: "Say it ain't so, Joe. Say it ain't so."

Although later acquitted of criminal charges, Jackson and seven of his teammates were banished from the sport for life by Judge Kenesaw Mountain Landis, the first commissioner of baseball, appointed as a result of the "Black Sox" scandal. With the game's reputation at stake, Judge Landis minced no words:

Regardless of the verdict of juries, no player that throws a ballgame; no player that undertakes or promises to throw a ballgame; no player that sits in a conference with a bunch of crooked players and gamblers where the ways and means of throwing games are planned and discussed and does not promptly tell his club about it, will ever play professional baseball.

Baseball is not banking. The national pastime is not the national currency. But change "throwing games" to "coin clipping" or "note shaving" and Judge Landis imposed a standard of conduct on baseball that would terminate the services of all the Fed's governors and most of their predecessors. Baseball's most recent scandal -- Sammy Sosa's corked bat -- is a reminder that human nature does not change, and that whatever their field of endeavor, even respected professionals require governance by rules that are effectively and impartially enforced.

Against all odds, the Revolution succeeded, but in the process the colonists learned the hard way about the dangers of paper money. The monetary provisions of the Constitution were designed and intended to spare future generations of Americans the hardship of reliving this experience, caustically captured in a common expression of the day: "Not worth a Continental."

Those who have put Fed chairman Greenspan on a pedestal neither contemplated nor authorized by the Constitution might ponder on this Independence Day whether their hero, too, may have feet of clay, and whether at some future date -- perhaps not too far distant -- they may have occasion to echo the disappointed young baseball fan of so long ago: "Say it ain't no Continental, Alan. Say it ain't worthless."