You are here

Chris Powell: The why and how of gold price suppression

Remarks by Chris Powell, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Standard Chartered's "Earth's Resources" Conference

J.W. Marriott Hotel, Hong Kong

Thursday, June 21, 2012

The Henley Group Client Seminar

Club Lusitano, Hong Kong

Thursday, June 21, 2012

Hong Kong Gold Investment Forum

Renaissance Harbour View Hotel, Hong Kong

Tuesday, June 26, 2012

This conference is important because gold long has been money and may again be the best and most important money. Most investment houses don't understand this; some of the few that do understand it fear to acknowledge it. But far from being a quaint antique, gold is actually the secret knowledge of the financial universe.

Gold is so important that Western central banks -- particularly the U.S. Treasury and its Exchange Stabilization Fund, the Federal Reserve, and allied central banks -- rig the gold market every day, even hour by hour. Why do they do this?

It's because gold is a powerful competitive currency that, if allowed to function in a free market, determines the value of other currencies and influences interest rates and the value of government bonds.

There is much academic literature supporting gold's influence over currencies, interest rates, and government bonds throughout history. Prominent in this literature is the study written by Harvard economics professor Lawrence Summers and University of Michigan economics professor Robert Barsky in the June 1988 edition of the Journal of Political Economy, a study titled "Gibson's Paradox and the Gold Standard." As with all the documents I'll cite today, the Summers and Barsky study is posted at my organization's Internet site, GATA.org:

http://www.gata.org/files/gibson.pdf

Summers went on to become treasury secretary of the United States, so his study of gold's influence on currencies, interest rates, and bond prices is pretty good authority. The Summers and Barsky study implied that governments could achieve their ideal of low interest rates and strong government bond prices by getting control of the price of gold.

Sona Discovers Potential High-Grade Gold Mineralization

at Blackdome in British Columbia -- 13.6g over 1.5 Meters

From a Company Press Release

November 22, 2011

VANCOUVER, British Columbia -- With its latest surface diamond drilling program at its 100-percent-owned, formerly producing Blackdome gold mine in southern British Columbia, Sona Resources Corp. has discovered a potentially high-grade gold-mineralized area, with one hole intersecting 13.6 grams of gold in 1.5 meters of core drilling.

"We intersected a promising new mineralized zone, and we feel optimistic about the assay results," says Sona's president and CEO, John P. Thompson. "We have undertaken an aggressive exploration program that has tested a number of target zones. Our discovery of this new gold-bearing structure is significant, and it represents a positive development for the company."

Sona aims to bring its permitted Blackdome mill back into production over the next year and a half, at a rate of 200 tonnes per day, with feed from the formerly producing Blackdome mine and the nearby Elizabeth gold deposit property. A positive preliminary economic assessment by Micon International Ltd., based on a gold price of $950 per ounce over eight years, has estimated a cash cost of $208 per tonne milled, or $686 per gold ounce recovered.

For the company's complete press release, please visit:

http://www.sonaresources.com/_resources/news/SONA_NR18_2011-opt.pdf

As it turns out, controlling the currency markets generally by rigging the gold market particularly is the most efficient mechanism of imperialism. There is much history of this. Indeed, rigging the currency markets was the primary mechanism by which Nazi Germany expropriated occupied Europe during World War II. Expropriation by force of arms was actually only a small part of the Nazi conquest. The rigging of the currency markets turned every citizen of an occupied country into an agent of the occupation every time he used money. This currency market rigging directed all production in the occupied countries into Nazi Germany and blocked any return flow. It enabled Nazi Germany to run without consequence the same sort of fantastic trade deficit lately run by the United States. The United States learned all about the Nazi expropriation of Europe through currency market rigging because it was documented by the November 1943 edition of the U.S. War Department monthly intelligence letter, Tactical and Technical Trends:

http://www.gata.org/node/10457

Exactly how do Western central banks and particularly the U.S. government rig the gold market?

They used to do it conventionally and in the open by dishoarding their gold reserves at strategic moments, and then by dishoarding their gold reserves regularly, every day, as the United States, United Kingdom, and seven of their Western European allies did during the 1960s through a public operation called the London Gold Pool. The London Gold Pool held the gold price at $35 per ounce until it collapsed in March 1968 under rising demand that drained the U.S. gold reserve from 25,000 tonnes down to just more than the 8,000 tonnes officially reported today:

http://en.wikipedia.org/wiki/London_Gold_Pool

After the collapse of the London Gold Pool the United States and its allies regrouped to figure out how to rig the gold market surreptitiously -- not just with dishoarding but also with the so-called leasing of gold; the issuance of gold derivatives, including futures and options; and, more recently, high-frequency trading undertaken through investment houses that were happy to serve as government's intermediaries in the gold market as they could front-run government trades. When the rigging is done surreptitiously like this, much less central bank gold has to be dishoarded and the dishoarding that is done has far more suppressive influence on the price.

But Western central bank market rigging goes far beyond gold. In an essay published in 2001 and titled "The Debasement of World Currency -- It Is Inflation, But Not as We Know It" --

-- the British economist Peter Warburton discerned that central banks were using investment banks to issue derivatives throughout the commodity futures markets to siphon away money that was looking for a hedge against inflation -- to siphon money away from the hoarding of real goods, hoarding that would have driven up consumer price indexes and made inflation plain to the markets and the public. These derivatives are essentially naked short positions that cannot be covered. Warburton concluded that the prerequisite of a hedge against monetary debasement would have to be some asset that was not associated with a futures market, like good farmland or clean water supplies. For as the saying goes: "The futures markets are not manipulated; the futures markets are the manipulation."

This market rigging by central banks and their intermediaries explains the great disparagement of gold: that, despite its tremendous price increase over the last decade, gold has not kept up with inflation since gold's last great rise around 1980. Somehow no one disparaging gold asks why it has not kept up with inflation. The answer is that gold derivatives have created a vast imaginary supply of gold for which delivery has not been demanded, most gold investors choosing to leave their gold purchases on deposit with the bullion banks that "sold" them the gold. As a result the world now has a fractional-reserve gold banking system that is leveraged in the extreme.

Yes, all commodity futures markets have created paper promises of supply that could not be covered by real product and have always been settled in cash. But most commodity markets are for goods that are to a great extent delivered and consumed. Gold is different, for gold is not consumed but rather hoarded, as a means of exchange, as money, and most gold purchased in the futures markets is never delivered at all but rather left on deposit with those financial institutions that purport to sell it. This system has produced a very disproportionate amount of imaginary, elastic, but undeliverable supply, even as people buy gold precisely because they assume that its supply is not elastic, that its supply is limited to total past production plus annual mine production.

That assumption is a terrible mistake.

You can get an idea of the vast imaginary supply of gold by reviewing the incomprehensibly huge gold and interest rate derivative positions attributed to the U.S. investment bank JPMorganChase in the reports of the U.S. Comptroller of the Currency. These derivative positions are almost certainly not MorganChase's own positions at all but, as GATA consultant Rob Kirby of Kirby Analytics in Toronto has written, rather U.S. government positions effected through MorganChase:

http://news.goldseek.com/GoldSeek/1249407911.php

After all, the U.S. Treasury Department's Exchange Stabilization Fund is expressly authorized by law to trade secretly in all markets, including the gold market, on the U.S. government's behalf. And the law expressly exempts the ESF from answering to anyone but the treasury secretary and the president:

http://www.treasury.gov/resource-center/international/ESF/Pages/esf-inde...

Gold market expert Jeff Christian of CPM Group testified to a hearing of the U.S. Commodity Futures Trading Commission on March 25, 2010, that the ratio of "paper gold" to real metal in the so-called London physical market may be as high as 100 to 1:

Christian provided a similar account 10 years earlier in his essay "Bullion Banking Explained":

And if leverage of 100 to 1 ever triggers a short squeeze, well, as Federal Reserve Chairman Alan Greenspan testified to Congress in 1998, "Central banks stand ready to lease gold in increasing quantities should the price rise":

http://www.federalreserve.gov/boarddocs/testimony/1998/19980724.htm

Greenspan did not give similar assurances about soybeans or pork bellies.

How can we prove this market rigging?

GATA has compiled and published at its Internet site copies of dozens of records. These include minutes of government agency meetings, interviews with government officials, declassified intelligence agency memoranda, and public statements and memoirs by central bankers:

http://www.gata.org/taxonomy/term/21

These documents are not mere speculation and "conspiracy theory." They are the evidence, proof, and acknowledgement of long-established government policy -- policy that used to be public and readily acknowledged, as with the London Gold Pool.

Some of these documents are quite current. For example, in a brochure distributed to central banks being recruited as members in 2008, the Bank for International Settlements even advertised its services intervening surreptitiously in the gold market to help rig currency markets generally:

http://www.gata.org/node/11012

Also among the records GATA has collected are admissions of gold market rigging -- yes, admissions -- from four former chairmen of the U.S. Federal Reserve -- William McChesney Martin, Arthur Burns, Paul Volcker, and Greenspan --

http://www.gata.org/node/10909

-- and the Netherlands central banker Jelle Zijlstra, who was simultaneously president of the Dutch central bank as well as the Bank for International Settlements:

http://www.gata.org/node/11304

It's hard to find better authority than these men.

To obtain some of these proofs, GATA has sued central banks and particularly the U.S. Federal Reserve, against which in 2011 we won a freedom-of-information lawsuit in U.S. District Court for the District of Columbia. The lawsuit produced a written admission by a member of the Federal Reserve Board of Governors, Kevin M. Warsh, that the Fed has secret gold swap arrangements with foreign banks and that the Fed cannot ever permit these gold swap arrangements to become public:

The only purpose of secret gold swap arrangements is secret intervention in the gold market.

Interestingly, last December, soon after resigning from the Fed’s Board of Governors, Warsh wrote an essay in The Wall Street Journal complaining about the new central bank policy called "financial repression." He asserted that government policymakers now are "finding it tempting to pursue 'financial repression' -- suppressing market prices that they don't like":

http://www.gata.org/node/10839

Warsh did not mention gold specifically, but gold was an obvious candidate for such suppression. Unfortunately three Wall Street Journal reporters refused my request that the newspaper question Warsh in pursuit of the big story he had just dropped in the newspaper's lap.

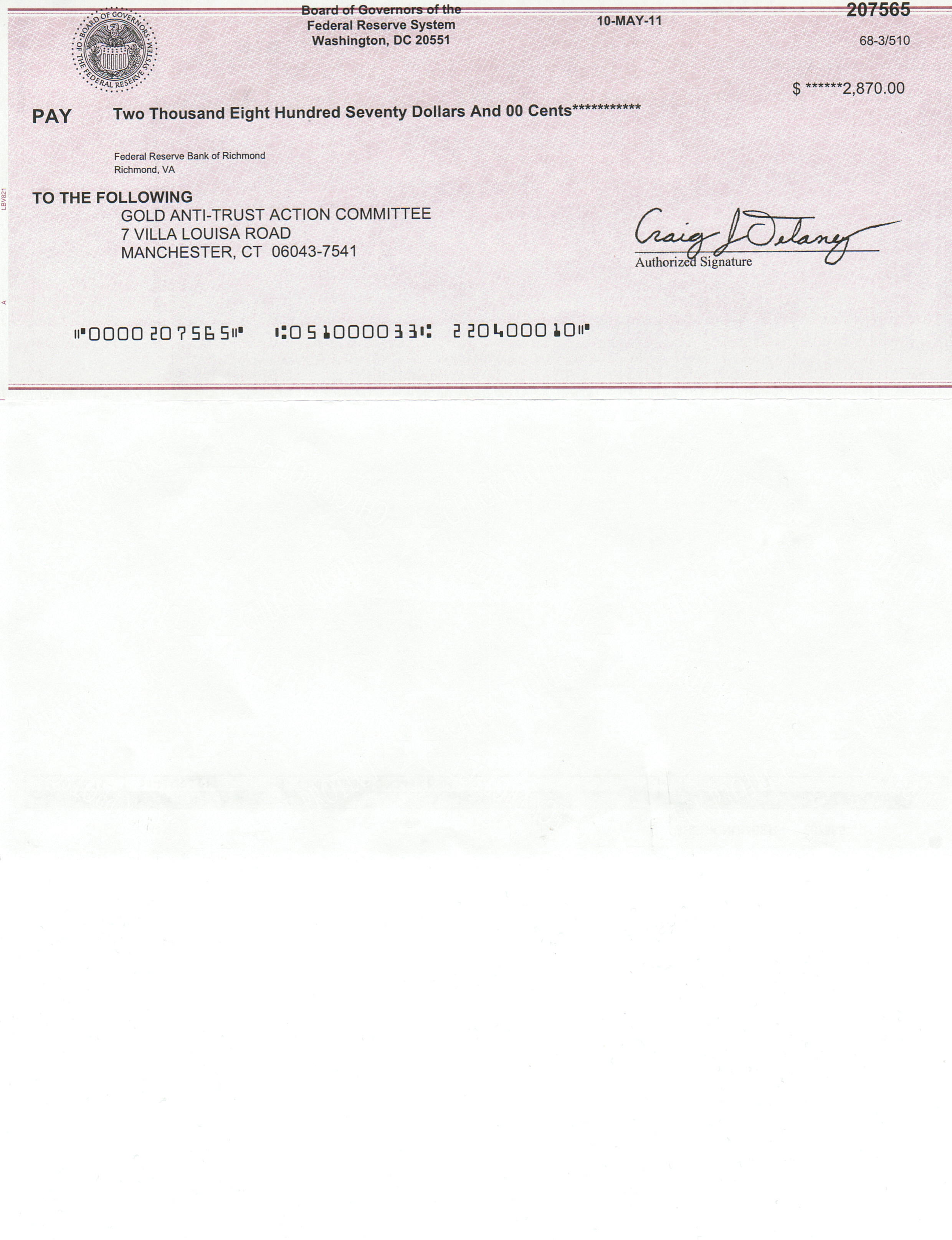

Since GATA beat the Fed in our freedom-of-information lawsuit, the court compelled the Fed to pay us legal costs. While the payment was only nominal, a check for $2,800, that check is a formal finding by a court that GATA is on to something and so the check too is posted at our Internet site:

http://www.gata.org/files/FedCheckLegalCosts.jpg

And since the court recognized the Fed's right to conceal most of its gold-related documents, in part because disclosure would reveal "proprietary" information about other banks, the lawsuit demonstrated that the Fed is keeping many gold-related secrets. Why should the Fed be allowed to have any secrets about gold?

GATA also has proven gold market manipulation by examining trading data, most notably in a study by our board member and market analyst Adrian Douglas showing that the gold price during trading in the London market has gone down steadily for 10 years even as the worldwide gold price has gone up steadily in that time. That is, anyone buying gold on the opening of the London market and selling it on the close every day over the last decade would have lost a huge amount of money even as the gold price rose steadily around the world:

https://marketforceanalysis.com/articles/latest_article_081310.html

The London Gold Pool of the 1960s suppressing the price continues to operate today, only with different mechanisms.

Why does all this matter?

It matters because rigging the gold market is part of a general scheme by which a secretive and unelected elite in the United States controls the value of all capital, labor, goods, and services in the world -- controls the value of everything. This is a totalitarian and parasitic system. It needs only to be exposed to be overthrown. But the mainstream financial news media in the West refuse to examine the documentation of this scheme and to put critical questions to central banks. Indeed, the first rule of financial journalism in the West is that central banks cannot and must not be questioned. As central banks intervene more and more to defeat markets, this rule makes most Western financial journalism simply irrelevant.

What are the investment consequences of this situation?

First, much if not most institutional investment gold and even central bank gold is only "paper gold," only imaginary, a claim against financial institutions that do not have on deposit all the gold to which they have issued claims. So there is a huge naked short position in the investment forms of gold around the world. If you don't have physical possession of your gold, or if it is not kept for you in "allocated" form outside the fractional-reserve gold banking system, your gold probably doesn’t exist and may not be available to you when you really want it.

Second, despite the silence in the West about gold market rigging, it is no secret in the East. Both the Russian and Chinese governments have issued public statements about it. That is, the Russian and Chinese governments know all about the Western gold market rigging scheme and are positioning themselves to profit from its end:

http://www.gata.org/node/10380

http://www.gata.org/node/10416

Third, gold investing is surrounded by political risk, including the risk of confiscation of both gold bullion and mining properties by desperate governments, the risk of prohibitive mining royalty requirements, and the risk of prohibitive capital gains taxes. Thus diversification in gold investing and gold location is vital.

And fourth, gold investing also offers the prospect of great reward upon a sudden official upward revaluation of gold. For example, a 2006 study by the Scottish economist Peter Millar concluded that central banks would need to raise the gold price by a factor of seven to 20 times in order to reliquefy themselves, devalue their currencies, and avert the sort of catastrophic debt deflation that is occurring today:

And the U.S. economists and investment fund managers Lee Quaintance and Paul Brodsky last month published a report asserting that central banks now likely are engaged in redistributing gold reserves among themselves in preparation for just such an upward revaluation of gold and for gold's return as formal backing for currencies:

http://www.gata.org/node/11373

But the purpose of all this market rigging is to suppress not only the price of gold but to suppress commodity prices generally. It is just the latest manifestation of the everlasting war of the highest levels of the financial class against the producing class, only this time the producing class hasn't yet figured out what's going on. Most tragically, much of the gold mining industry itself doesn't understand what is being done to it -- doesn't understand that it's not just digging metal out of the ground but minting money and competing with all other issuers of money and that this competition is far more cutthroat than imagined.

GATA hopes to change that.

If you are unable to locate something at GATA's Internet site, please e-mail me at CPowell@GATA.org and I'll help you. And if you find GATA helpful, please consider making a financial contribution to us:

We're a non-profit educational and civil rights organization sustained only by donations from believers in free and transparent markets. With enough financial support I'll be able to go home, and maybe even come back here again to keep spreading the word.

Join GATA here:

Toronto Resource Investment Conference

Thursday-Friday, September 27-28, 2012

Toronto Sheraton Centre Hotel

Toronto, Ontario, Canada

http://www.cambridgehouse.com/event/toronto-resource-investment-conference

New Orleans Investment Conference

Wednesday-Saturday, October 24-27, 2012

Hilton New Orleans Riverside Hotel

New Orleans, Louisiana

http://www.neworleansconference.com/

* * *

Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006:

http://www.goldrush21.com/order.html

Or by purchasing a colorful GATA T-shirt:

Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009:

http://gata.org/node/wallstreetjournal

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

Prophecy Platinum Announces Wellgreen Preliminary Economic Assessment:

38% Pre-Tax IRR, $3.0 Billion NPV, and a 37-Year Mine Life

Company Press Release

VANCOUVER, British Columbia, Canada -- Prophecy Platinum Corp. (TSX-V: NKL, OTC-QX: PNIKF, Frankfurt: P94P) reports the results of an independent NI 43-101-compliant preliminary economic assessment for its fully owned Wellgreen nickel-copper-platinum group metals project in the Yukon Territory.

The independent assessment, prepared by Tetra Tech, evaluated a base case of an open-pit mine (with a mining rate of 111,500 tonnes per day), an on-site concentrator (with a milling rate of 32,000 tonnes per day), and an initial capital cost of $863 million. The project is expected to produce (in concentrate) 1.959 billion pounds of nickel, 2.058 billion pounds of copper, and 7.119 million ounces of platinum, palladium, and gold during a mine life of 37 years with an average strip ratio of 2.57.

The financial highlights of the preliminary economic assessment, shown in U.S. dollars, are as follows:

Payback period: 3.55 years

Initial capital investment: $863 million

IRR pre-tax (100% equity): 38 percent

NPV pre-tax (8% discount): $3 billion

Mine life: 37 years

Total mill feed: 405.3 million tonnes

Mill throughput: 32,000 tonnes per day

Prophecy Chairman John Lee says: "We are pleased with the preliminary economic assessment results. The numbers indicate that Wellgreen is one of most exciting mineral projects in the Yukon. The company is drilling to upgrade and expand the resource base. The infrastructure is excellent as the project is only 1,400 meters in altitude and 14 kilometers from the paved Alaska Highway, which leads to the Haines deep seaport. Discussions are under way with support from local stakeholders regarding permitting and logistics."

For the complete press release, please visit:

http://prophecyplat.com/news_2012_june18_prophecy_platinum_announces_res...

{kind=link}